Europe, through the Green Deal expressed its ambition to be the first continent to become climate neutral by 2050, with Europe aiming to achieve net zero greenhouse gas emissions. But how do you actually measure how much greenhouse gas emissions your company emits, and what is Titeca doing to reduce its emissions?

ESG - E in the spotlight

European legislation around sustainability reporting (CSRD) aims to share information about a company's ESG performance. ESG includes the 3 pillars of "Environmental," "Social" and "Governance." Under ESG, companies can explain their environmental, people and good governance efforts.

In this article, we take a closer look at the environmental (E) pillar, which consists of 5 main themes:

- Climate

- Pollution

- Water and marine resources

- Biodiversity and ecosystems

- Resource use and circularity

Combating climate change is a very hot and pervasive topic. Therefore, the focus of this article is on reporting on emissions, with the underlying objective of setting targets to reduce these emissions to combat climate change.

Report on your company's emissions

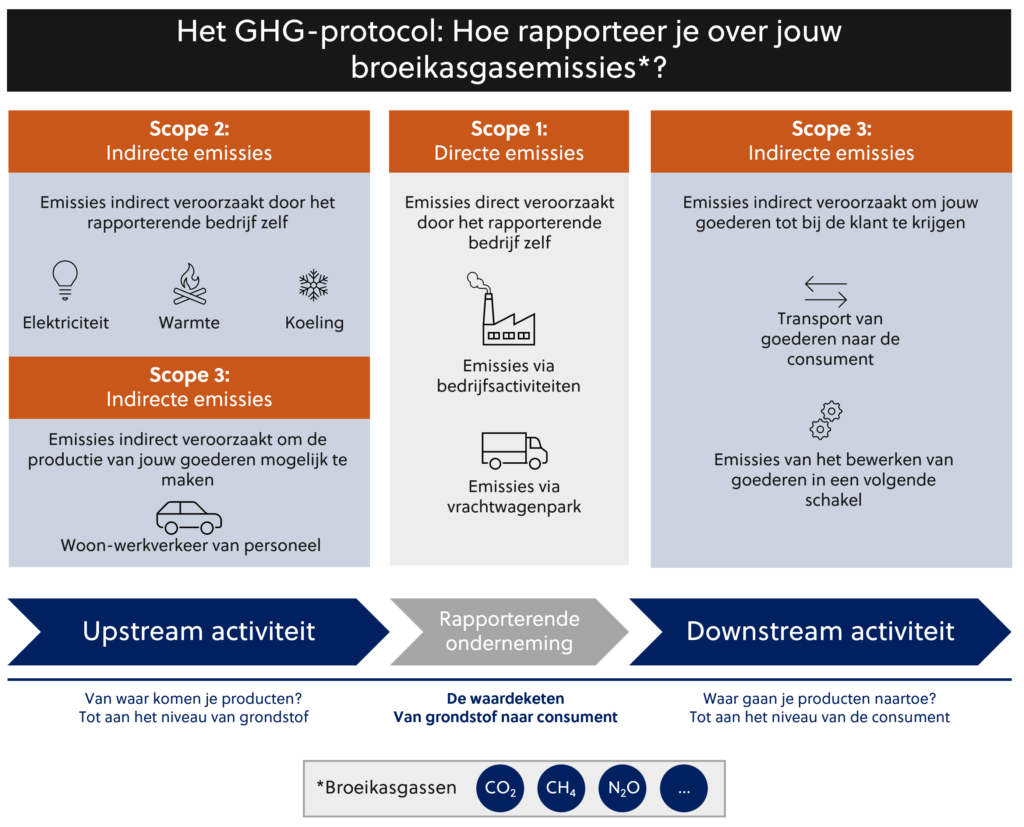

The CSRD legislation relies on existing legislation for a number of specific reporting points. When companies report on their efforts to mitigate climate change, they must map their greenhouse gas emissions through the methodology described in the GHG Protocol, in which a company reports on its so-called scope 1, scope 2 and scope 3 emissions.

The GHG Protocol maps your company's emissions across the entire value chain. Not only the direct emissions caused by e.g. fuel combustion of your vehicle fleet are taken into account, but also all indirect emissions such as the commuting of your staff. For example, an employee must first travel to your company to work. During this transportation, he will emit greenhouse gases that are included in your company's total emissions.

Indirect emissions are located prior to the production of your goods (upstream in the value chain), but also after the production of the goods (downstream in the value chain). For example: getting your product to the customer requires transportation. These emissions also belong to your total greenhouse gas emissions.

Below we would like to give you a diagram with some examples for the different types of scopes and (in)direct emissions throughout the value chain. The examples given are not exhaustive.

How does Titeca Pro Accountants & Experts limit its emissions?

Titeca Pro Accountants & Experts is firmly committed to sustainability with its transition to an all-electric fleet. In a conversation with fleet colleagues Barbara Sergeant and Lien Vandecaveye, it becomes clear that this move stems from embedding sustainability within Titeca's corporate vision.

The road to making the fleet more sustainable had many steps, from selecting electric vehicles to setting up a complete charging infrastructure. Looking to the future, the duo highlights Titeca's ambitious goals: by the summer of 2029, all company vehicles will be electric, complemented by a bicycle leasing program for greener mobility. Through this path, we are not only striving for a more sustainable society, but also want to promote inspiring entrepreneurship.

Are you like us all the way pro sustainability? Then check out our sustainability page.

Do not hesitate to contact us here contact us with questions.

Would you like to proactively address this issue so that you too can make an impact to create a more sustainable world? Then make an appointment with our pro experts here!